Know all about your Credit Worthiness at Samadhan Kender

Know all about your Credit Worthiness at Samadhan Kender

September 23rd, 2021

September 23rd, 2021

Enter Your Email

What is Credit Score and Credit Rating Agency:

Credit Score is a numerical value calculated by an approved credit rating agency to provide report about credit worthiness of any individual. CIBIL ( Credit Information Bureau India Ltd. is the best credit rating agency and all the nationalized bank and private sector banks rely upon the Credit Score rating provided by CIBIL. Other upcoming and less know rating agencies operating in India are Equifax and Experian.

What is the importance of Score based Credit Rating:

Any prospective borrower must check his or her credit score before approaching any bank for any type of loan so that his or her application does not get rejected because of poor or defective credit rating score. Samadhan Kender not only provides services to know your credit score before hand but also helps the prospective borrowers to get the score improved or rectified as sometimes the bad score computed by CIBIL is due to non reporting or wrong reporting by the banks and financial institutions.

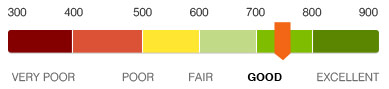

What is Good or Bad CIBIL Score:

Normally CIBIL score is a 3 digit number ranging from 300 to 900 and score more than 750 is considered good score to approach the bank for availing loan. If you have score less than 750 then you need professional advice being provided by Panel of Experts at Samadhan Kender, who will analyse your credit rating report and suggest the ways to improve the credit score in short duration. CIBIL scores are updated on monthly/quarterly basis.

What can be the possible factors for poor Credit Score:

- Normally people go to one bank or the other for their credit needs and the lending institutions, as a matter of abundant caution, draw the credit score in the first instance. In case the bank declines the loan applications for other reasons like non availability of adequate security, margin or owned capital then the inquiries made by the lenders get registered in your database with CIBIL. While approaching the bank either get your score based report through Samadhan Kender or yourself to show it to the bank as reports taken out privately will not downgrade you credit score whereas inquires by banks can downgrade your credit score as the computing systems will mark you as “Credit Hungry” who is in urgent need of money. If you approach one bank after another every banker’s inquiry will lower your credit score with the new bank increasing the chances of your application getting rejected. So, it is prudent to obtain the credit rating score privately from Samadhan Kender or elsewhere.

- If your credit score shows high current balances and borrowings the bankers will become alert as it will tell the bankers about your repaying capacity based on your income as per your IT returns. It is therefore, advisable to close the overdraft limits with credit balances, adjust the loans against bank deposits etc. etc.

- Sometimes even after you repay the loan in full the banks do not close the loan accounts and such loan accounts are shown “Open Status” in your credit score. Experts at Samadhan Kender will help you at every step to get the status changed from “Open” to “Closed” as open status may mislead the lending institutions.

- Similarly sometimes loan accounts in your credit report may be reported with status as “Written Off” or “Settled”. It is always better to negotiate with the lending institutions to get the status changed to closed as the written off or settled status are likely to raise the risk perception and result in negative impression.

- Moreover even if you clear your defaults and over dues then it is not going to improve your credit score immediately and you have to keep a clean track to have better credit score.

- While repeated bank inquiries can lower your credit score but having a Credit Card and using it judiciously can improve your Credit Score.

What is the time limit to wipe out defaults in the Past:

- Your Credit History is preserved for at least 7 years from the date of maturity of loan and it can be stretched even beyond 7 years.

- Even if you have paid your loan in full there is default of single loan installment then it will go on reflecting in your credit score for 7 years after the repayment in full.

For further information visit Samadhan Kender, near Bikaner Mishtan Bhandar, Rajpura-Patiala Road, Rajpura 140401 Punjab.

As I’m unable to add image to this post, I will try to show you the image in text from…